Is Turmoil the only Oil left for the Mechanics of Economy?

The Economic Survey of India 2025-26 presented on 29th Jan had highlighted how India’s GDP Growth can be hampered by a combination of elements like Financial Stress, trade frictions and geopolitical tensions. It stated how the world will be in constant state of turmoil and the key will be less about continuity but more about managed disorder.

Lo and behold, just as one month passes by after the economic survey, we have countries in the Middle East scurrying to war. As India watches by, it brings nothing but more friction to an already dull investment climate.

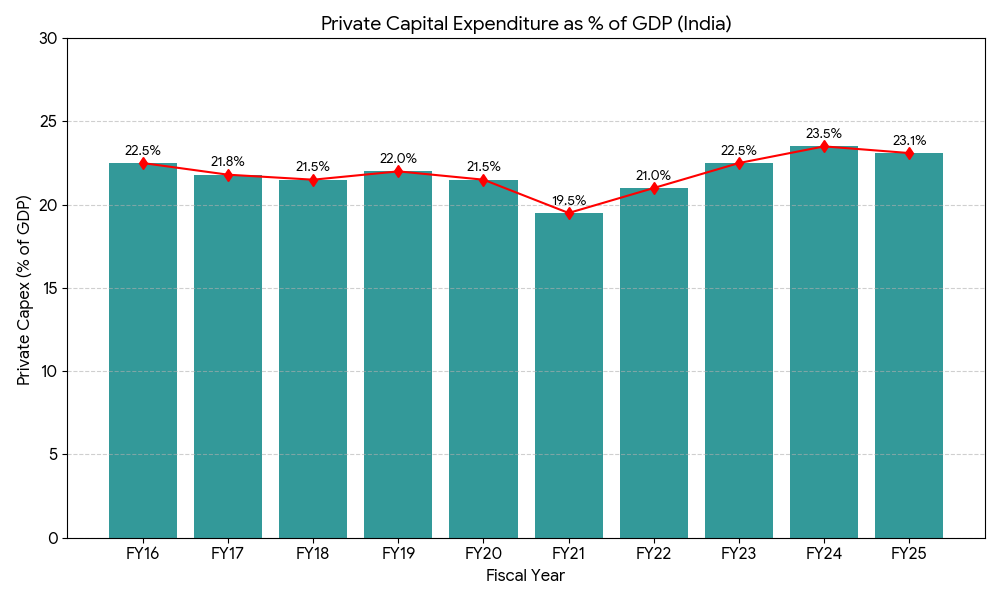

Stagnant Private Capex

Despite the government’s record breaking public capex estimated at 4.4% of GDP for FY27, private sector participation remains muted, it has been stagnant hovering around ~23% of total Gross Fixed Capital Formation (GFCF) for a long time. For emerging and developing economies like us which need to create more jobs to in turn drive consumption, this remains the missing engine.

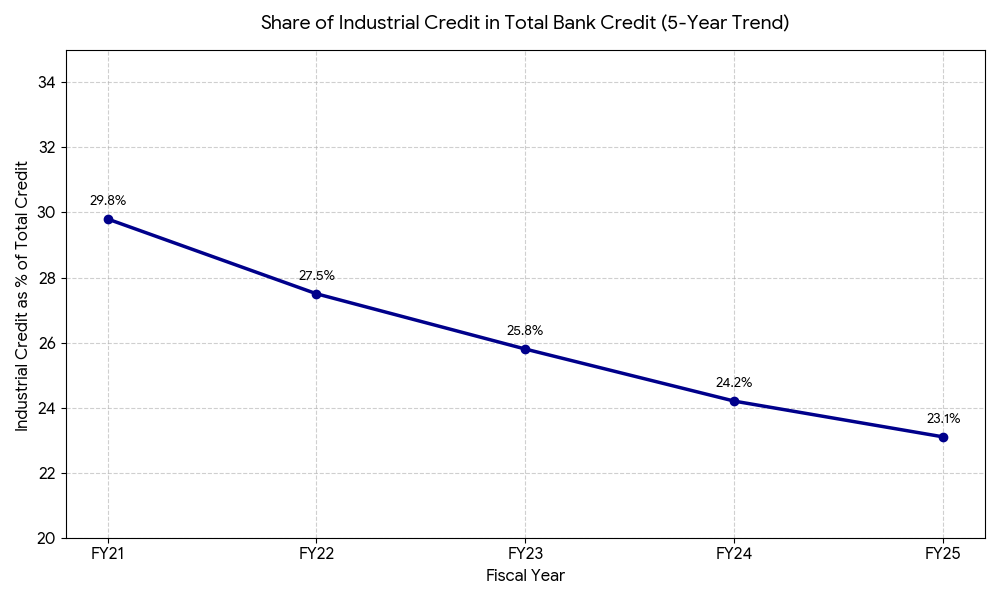

Credit Cooling

Along with immediate Capex, companies also seem to be pulling away from creating capacity or projects in the near future, largely deleveraging and using idle cash for buybacks instead of creating IP assets. The share of industrial credit is declining while the share of unsecured personal credit is increasing in the economy. Banks have pivoted heavily toward retail loans (housing, personal loans) and the services sector. This shift reflects a cautious approach by both lenders and borrowers in the industrial segment.

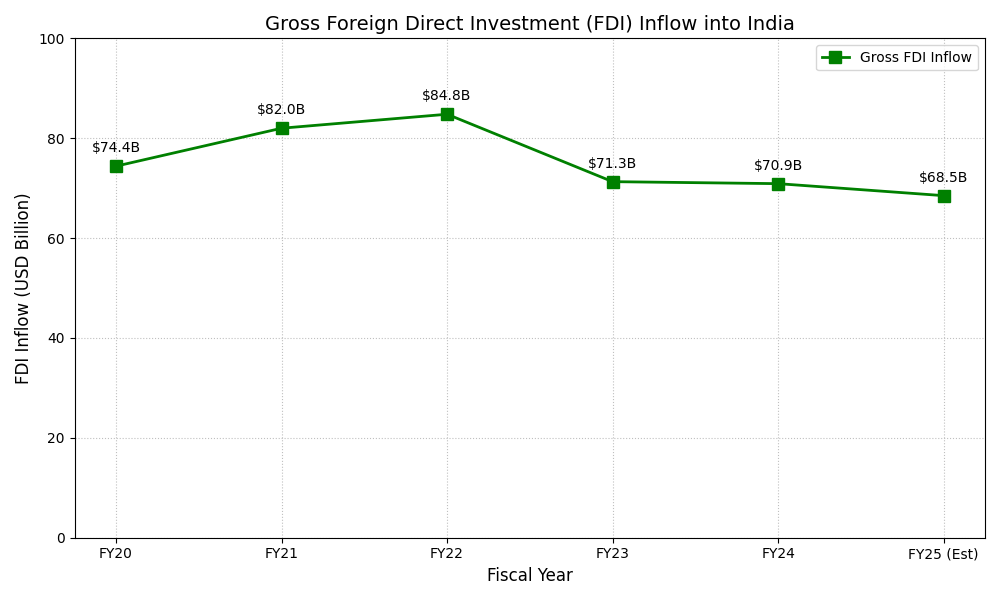

The Global Retreat of FDI

While FPI in a country is less sticky and prone to flight, FDI is considered to be more sticky & unfortunately FDI in India has also not moved much in spite of recent interventions like PLI schemes and tax breaks offered heavily under Made In India. The beneficiary of China plus one strategy seem to be other countries in Asia notably Thailand and Vietnam while China is moves away from heavy machinery towards the new three sectors- Electric Vehicles, Lithium Batteries and Solar Products. South Korea has been moving forward in hardware required for AI infrastructure to be competitive against it’s peers in China and Taiwan.

The Unlikely Victims of Connected World Order

The unlikely victims of this interconnected world order seem to be far and wide. In countries elsewhere of Middle East- the tremors were felt in KOSPI index crash which is the Korean Stock Market index heavily influenced by Samsung and SK Hynix which manufacture RAM and power most of the AI infra that we see today and which was affected in response to Amazon Data Centers damaged in the war.

The other distant victim seems to be the sale of Indian Premium Spirits which have shown nearly flat sales growth even while the domestic market seems to flourish and preimmunize endlessly. While Indian travelers are increasing, a global downturn in discretionary spending at Western airports has stunted the international breakout of Indian luxury brands.

The Silver Lining

The prospects of continuous and ongoing proxy as well as real wars have prompted some companies to onshore even in the face of FTA’s being signed, because let’s face it, in this fragile world, nothing is permanent. The biggest bet that I read of in recent times seems to be the inauguration of the INR 9,000 Cr. Jaguar Land Rover plant in Tamil Nadu by Tata Motors which is betting big on the Indian Market.

Conclusion

The economy and the companies now have to move beyond operating efficiency towards optionality & trade offs. On-shoring, creating multiple sources and capacity plug ins will ultimately make it costlier for the consumer to buy all products in general. The increase in Oil prices with a war premium will surely cascade down to energy prices in EU and India further. The Indian economy’s era of low inflation and high growth rates will come into doubt, making it harder for the government to spend on Public Infrastructure as well as for RBI to support the already fragile rupee tumbling down against the dollar. May the guns fall silent, may we embark again on a journey of glorious peaceful growth.